Tax Benefits for NRI Investors: Leveraging Real Estate Assets in North-East Bangalore

Tax benefits for NRI investors in India provide powerful avenues to lower tax liabilities, maximize rental yields, and protect wealth when leveraging high-growth real estate assets in North-East Bangalore. Known for its booming airport corridor, tech parks, and mega-townships, North-East Bangalore—spanning areas like Hebbal, Hennur, Thanisandra, and Budigere Cross—has become a prime destination for Non-Resident Indians (NRIs). By understanding the tax codes updated in the Union Budget, global Indian investors can turn these real estate assets into highly tax-efficient, profitable portfolios.

The Growth Engine of North-East Bangalore

Before looking at the tax codes, it helps to understand why North-East Bangalore is so popular with NRI investors. This corridor acts as the main bridge between the city's central business districts and the Kempegowda International Airport.

Driven by the expansion of the Namma Metro Phase 2B, the upcoming Peripheral Ring Road (PRR), and massive employment zones like the Aerospace SEZ and Manyata Tech Park, property values here are growing at a rapid pace. This mix of fast capital appreciation and high rental demand creates an ideal setup for NRIs looking to optimize their tax strategies.

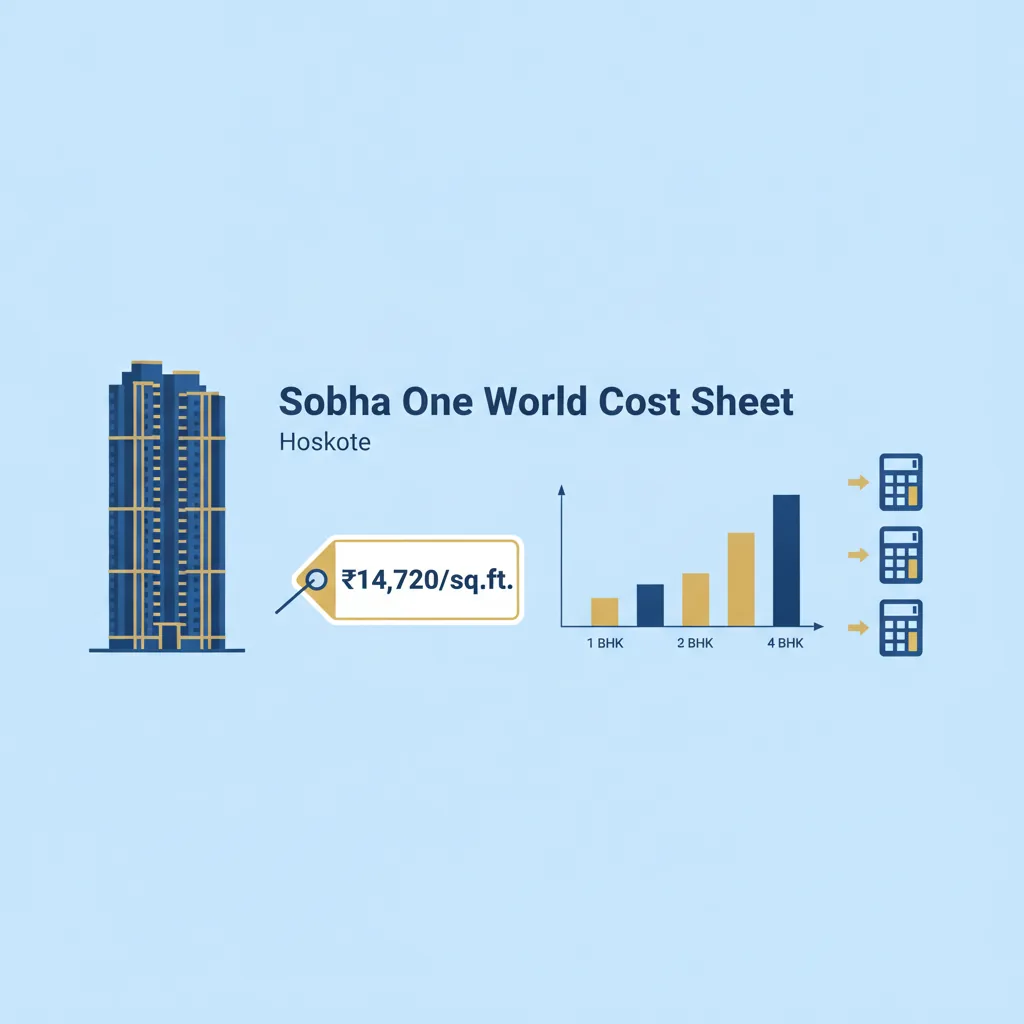

Submitting an early investment in large-scale flagship properties, such as the massive 300-acre Sobha One World township located right along this high-growth growth belt, allows global investors to secure premium high-rise assets at lower entry rates, compounding their long-term yields.

4 Major Tax Benefits for NRI Landlords and Buyers

The Income Tax Act provides NRIs with several deductions that can lower taxable property income in India down to minimal amounts.

1. The 30% Flat Standard Deduction on Rent

NRIs who lease out their apartments or villas in North-East Bangalore do not pay tax on the full rental amount they collect. Under Section 24(a), the government grants a flat 30% standard deduction on total annual rental income to cover basic repairs and property upkeep. This deduction is allowed automatically, regardless of how much you actually spent on maintaining the property.

2. Home Loan Interest Deductions

If you use an NRI home loan to purchase a premium property in this corridor, you can claim significant deductions under Section 24(b):

- For let-out properties (rented homes), the entire interest amount paid on the home loan during the financial year can be deducted directly from your taxable Indian income.

- For self-occupied properties (kept for personal vacations), you can deduct up to ₹2 Lakhs in interest payments every year.

3. Deductions on Principal Repayments

NRIs can also lower their taxable income by claiming the principal component of their home loan repayments under Section 80C, up to a maximum limit of ₹1.5 Lakhs per year. This section also allows you to deduct the cost of stamp duty and property registration fees paid during the year of purchase.

4. Capital Gains Tax Exemptions on Resale

If you hold a real estate asset in North-East Bangalore for more than 24 months, it qualifies as a Long-Term Capital Asset. Under the tax rules, long-term capital gains are taxed at a flat 12.5% (without indexation). However, NRIs can legally avoid paying this tax entirely by reinvesting their profits through key channels:

- Section 54: Reinvest the capital gains into buying up to two new residential properties in India.

- Section 54EC: Reinvest the profits into specific government-notified bonds (like NHAI or REC) within 6 months of the property sale, up to a maximum cap of ₹50 Lakhs.

Streamlined Compliance Under Recent Tax Rules

The tax process for property transactions involving NRIs has become much simpler:

- No More TAN Hassles for Buyers: Resident buyers purchasing real estate from an NRI are no longer required to get a separate Tax Deduction Account Number (TAN) just to submit the required Tax Deducted at Source (TDS). They can now use a standard, straightforward PAN-based challan, making property sales much quicker and smoother for NRI sellers.

- DTAA Safeguards: India's extensive Double Taxation Avoidance Agreements (DTAA) with over 85 nations ensure that NRIs do not pay tax twice on the same rental income or capital gains in their home country and India.

Frequently Asked Questions

1. What are the key tax benefits for NRI investors in North-East Bangalore?

NRI investors can claim a flat 30% standard deduction on rental income, deduct their home loan interest and principal repayments from taxable income, and completely avoid long-term capital gains tax by reinvesting profits under Sections 54 and 54EC.

2. How is rental income from a property in Bangalore taxed for an NRI?

Rental income is taxed under your applicable Indian income tax slab rates. However, before calculating the tax, you can deduct a flat 30% standard deduction for maintenance, along with any local municipal property taxes and home loan interest payments.

3. What is the current Long-Term Capital Gains (LTCG) tax rate for NRIs?

If an NRI holds a residential property for more than 24 months, the profit from its sale is treated as a long-term capital gain and is taxed at a flat rate of 12.5% without indexation benefits.

4. Can an NRI avoid paying capital gains tax when selling a property?

Yes. An NRI can claim complete exemption from capital gains tax by reinvesting the net profit into another residential house property in India (under Section 54) or by investing the gains in government capital gains bonds within 6 months (under Section 54EC).

5. What is the new rule for TDS compliance when an NRI sells property?

Buyers purchasing property from an NRI no longer need to apply for a separate TAN to process the TDS. They can simply complete the entire tax deposit process using a standard PAN-based challan system, making the transaction faster and reducing paperwork.

6. Can an NRI use the Double Taxation Avoidance Agreement (DTAA) to save on taxes?

Yes. If the rental income or capital gains from your North-East Bangalore property are taxed in India, you can use DTAA provisions to claim a tax credit in your country of residence, ensuring you do not pay tax twice on the same money.

7. Is it necessary for an NRI to file an income tax return (ITR) in India for property investments?

Yes, filing an ITR is highly recommended. Even if your total Indian income falls below the taxable threshold, filing a return allows you to claim refunds on any excess TDS deducted by your tenants or property buyers.